Description

Eight Developments placed Central Point directly on Central Park in New Capital’s Financial and Business District. The project consists of ground floor plus twelve upper floors, with commercial units on the lower three levels and administrative space above.

The minimum investment starts at 1,088,000 EGP, with payment plans stretching up to ten years and rental guarantees during the initial period. The location sits within walking distance of planned government buildings and cultural institutions, which matters if you’re evaluating commercial viability in a district that’s still populating.

This isn’t about promotional language or investment hype. What follows is a practical examination of where Central Point sits, what the numbers actually mean, who this project genuinely suits, and what you should verify before committing capital.

Where Central Point Actually Sits?

Central Point occupies a plot in the Central Park area of New Capital’s Financial and Business District. The site has a 200-meter frontage on Central Park itself, plus a main street with 75 square meters of frontage.

Downtown New Capital sits roughly ten minutes away. The Government District and Ministries Quarter are both accessible within a short drive. The Presidential District falls within similar proximity.

Access comes through the Green River corridor and the northern Bin Zayed axis. These aren’t secondary roads but planned arterial routes designed to handle the district’s eventual traffic volumes when government offices and businesses fully occupy the area.

Al Massa Hotel and the Opera House are nearby, both institutional anchors that signal the character of the surrounding development. Central 33 Mall and Mall 88 Hub sit close enough to create a commercial cluster rather than leaving Central Point isolated.

The government’s commitment to relocating ministries provides some demand certainty for commercial and administrative space. Civil servants, business visitors, and residents of surrounding compounds will need services within reasonable distance. Whether that demand materializes on the timeline developers anticipate remains the central question for any New Capital commercial investment.

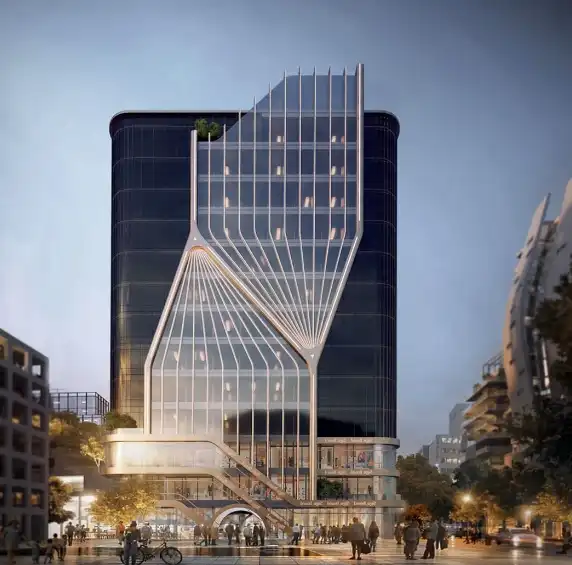

Building Design and Floor Distribution

Central Point rises thirteen levels: ground floor plus twelve upper floors. Eight Developments allocated most of the plot to landscaping, with the building occupying a smaller footprint than many competing projects. This creates more open space around the structure.

Commercial units in Central Point take the ground, first, and second floors. This placement makes sense for retail, cafes, and service businesses that depend on visibility and foot traffic from street level. Administrative units occupy floors three through twelve, separating office environments from retail activity.

The building uses elevators and escalators to manage vertical movement between floors. Four parking levels handle vehicle storage, which matters significantly in New Capital’s current car-dependent environment. Public transportation remains limited, so most visitors arrive by private vehicle.

Eight Developments has completed similar projects in the area, including Mall 88 Hub and The Strip Mall. Both follow comparable design principles, which provides some track record for evaluating execution capability.

The developer of Central Point New Capital hasn’t specified which construction firms handle which aspects of the build. Investors concerned about construction quality should visit completed Eight Developments projects to assess finishes and building systems firsthand.

Unit Sizes and Configurations

Spaces in Central Point start at 32 square meters for the smallest commercial units. Pharmacy spaces measure 95 square meters with an additional 14 square meters of outdoor area.

A 32-square-meter unit works for a mobile phone shop, currency exchange, or small café. Larger spaces suit pharmacies, professional offices, or clinics that need reception areas and private rooms.

Administrative units in Central Point New Capital vary in size to match different organizational needs. A small consultancy might take a single unit, while a law firm could combine adjacent spaces for a larger footprint.

Corner units typically offer better natural light and visibility from two sides, which affects both daily usability and eventual resale value. Interior units on upper floors cost less but receive less natural light and have no street presence.

Floor plans show internal divisions, though specific layouts vary by floor and position. Unit dimensions matter more than square meter totals. A poorly proportioned 50-square-meter space can be less functional than a well-designed 40-square-meter unit. Request detailed plans before committing.

Pricing Breakdown by Floor and Type

Pricing in Central Point Mall New Capital follows standard commercial real estate logic where ground-floor retail commands premium rates and prices decrease with height.

Ground floor commercial units range from 100,000 to 140,000 EGP per square meter. First-floor commercial spaces drop to 60,000–105,000 EGP per square meter. Second-floor commercial units price between 55,000 and 95,000 EGP per square meter.

Administrative units cost significantly less, ranging from 34,000 to 39,000 EGP per square meter. This reflects lower foot traffic and reduced visibility compared to street-level retail.

The minimum total investment of 1,088,000 EGP likely represents a small upper-floor unit around 32 square meters. Investors planning ground-floor retail should expect total costs several times higher.

These figures position Central Point in the middle range for New Capital commercial projects. Some competing developments in the Financial District charge more based on different locations or specifications. Others in less central areas cost less but offer reduced visibility and accessibility.

Price per square meter tells only part of the investment story. Total return depends on rental demand, which remains somewhat speculative while New Capital continues populating. The government’s ministry relocation provides some demand certainty, but the timeline for full occupancy and market-rate rents isn’t guaranteed.

Payment Plans and What the Numbers Actually Mean

Eight Developments offers three primary payment structures for Central Point:

- 10% down payment with the balance over seven years. This option includes a 35% return on the down payment over three years, with mandatory rental at 25–30%.

- 15% down payment with installments over eight years. This provides a 30% return on down payment over three years, with the same mandatory rental percentage.

- 20% down payment with the balance over seven years. This offers a 25% return on down payment over three years, again with 25–30% mandatory rental.

- These rental guarantees require careful examination. A 35% return over three years on the down payment doesn’t equal a 35% return on total investment.

On a 1,088,000 EGP unit with 10% down (108,800 EGP), a 35% return means approximately 38,080 EGP over three years, or roughly 12,693 EGP annually. That’s about 3.5% annual return on total investment during the guaranteed period, not 35%.

Facilities and Building Operations

- Central Point New Capital includes standard commercial building amenities rather than exceptional features.

- Central Point Mall New Capital incorporates retail space on lower floors, restaurants and cafes for food service, and meeting rooms for business use. High-speed internet throughout the building supports office operations.

- Security measures in Mall Central Point New Capital include surveillance cameras, security personnel, and controlled entry systems. Fire suppression systems meet code requirements.

- The building operates on a smart access system to manage entry and exit. ATMs facilitate financial transactions without requiring visitors to leave the complex.

- Maintenance and cleaning services in Central Point New Capital Mall keep common areas functional. The four parking levels provide vehicle storage, essential given New Capital’s current transportation limitations.

- One distinctive feature is a 9D fountain in the common areas, which serves as a visual attraction.

- These facilities represent baseline expectations for a modern commercial building. They ensure the building functions properly but don’t necessarily differentiate Central Point from competing projects in the same district.

- The operational model matters long-term. Whether Eight Developments retains management control or transfers it to a property management company affects service quality over time. Clarify the long-term management structure before purchasing.

Who This Project Actually Suits?

Central Point makes sense for specific investor profiles, not everyone looking at New Capital commercial real estate.

The project works for investors who believe New Capital will achieve its planned population and economic activity levels. If the government successfully relocates ministries and the district attracts private sector businesses, demand for commercial and administrative space should follow naturally.

Buyers with medium-term investment horizons—five to ten years—align better with this project than those seeking immediate returns. The area needs time to populate and establish rental rate benchmarks.

The extended payment plans suit buyers who want to deploy capital gradually rather than committing large sums upfront. This approach works if you’re building a portfolio across multiple projects or preserving liquidity for other opportunities.

Central Point Mall doesn’t suit investors expecting quick flips or immediate high rental yields. The area is still developing, and speculative gains depend entirely on the district’s successful maturation, which isn’t guaranteed on any specific timeline.

Comparing Central Point to Other Financial District Projects

Central Point enters a competitive field of commercial projects in New Capital’s Financial District. Mall 88 Hub and The Strip Mall, both by Eight Developments, offer similar concepts nearby. Central 33 Mall provides another comparison point.

The primary differentiator is the Central Park frontage, which provides visibility and a more pleasant immediate environment than projects facing only streets or other buildings. Whether this translates to higher rental rates or occupancy depends on how the district develops.

Pricing sits in the middle range. Some newer projects charge premium rates based on updated designs or different micro-locations. Earlier developments may offer lower entry points but with less modern specifications or less favorable locations.

Eight Developments’ track record with multiple New Capital projects suggests operational competence and financial stability to complete construction. Newer developers entering the market may offer attractive terms but carry higher execution risk if they lack a completion history.

What to Verify Before Committing

Several factors warrant attention before purchasing a unit in Central Point New Capital.

New Capital remains partially speculative. Government relocation is proceeding, but the pace and completeness of the move affect commercial viability directly. If ministries relocate with smaller staff numbers or maintain significant Cairo operations, demand projections may not materialize fully.

Construction timelines in large-scale developments sometimes extend beyond initial estimates. Clarify delivery dates in the contract and understand what penalty clauses exist for delays. Vague delivery language should raise concerns.

The rental guarantee system requires detailed documentation. Understand exactly what income the developer promises, under what conditions, for how long, and what recourse exists if they don’t meet obligations. Get this in writing as part of the purchase contract.

Tax implications for commercial property in New Capital should be reviewed with an accountant familiar with Egyptian real estate investment structures. Different ownership structures have different tax treatments.

Frequently Asked Questions About Central Point

Does the Central Park frontage actually improve commercial performance?

The park frontage provides visibility and a more attractive immediate environment than projects facing only streets. This matters for businesses that benefit from foot traffic and customers who prefer pleasant surroundings. However, actual commercial success depends on the broader district’s population density and economic activity. The park frontage is an advantage but not a guarantee of superior returns compared to well-located projects on major streets with higher traffic volumes.

What happens when the mandatory rental period ends?

After the guaranteed rental period ends—typically three years—unit owners can continue with property management services, find their own tenants, or occupy the space themselves. Rental rates will then reflect actual market conditions rather than guaranteed percentages. If the district has matured successfully, market rates may exceed guaranteed rates. If development lags, you may face lower occupancy or rental income than the guaranteed period provided.

Can I modify the unit’s interior after purchase?

Most commercial developments allow interior modifications within structural limitations. You typically cannot alter load-bearing walls, building systems, or the exterior facade. Interior partitions, finishes, and fixtures can usually be customized to suit your business needs. Confirm specific modification policies with Eight Developments before purchasing, and factor renovation costs into your total investment if you plan significant changes.

How does this compare to investing in established Cairo commercial areas?

Established Cairo districts offer immediate rental demand and proven market rates, but at higher entry prices and lower growth potential. Central Point requires accepting development risk in exchange for lower entry costs and potential appreciation if New Capital succeeds as planned. Cairo properties provide more liquidity and easier management. New Capital properties offer higher potential returns but with longer holding periods and more uncertainty about timing.

Conclusion

Central Point represents a calculated investment in New Capital’s developing Financial District rather than a guaranteed opportunity. The project’s Central Park location, structured payment plans, and rental guarantee system provide certain advantages for investors with appropriate timelines and risk tolerance.

The development makes most sense for buyers who believe in New Capital’s long-term trajectory, can accept several years of below-market returns during the district’s maturation, and don’t need immediate liquidity. The extended payment terms allow gradual capital deployment, while the rental guarantee provides some income certainty during the critical early years.

Eight Developments’ track record with similar projects in the area suggests competent execution, though no developer’s guarantees are absolute. The pricing positions Central Point in the middle range of New Capital commercial offerings—neither the cheapest entry point nor the most premium option.

Success ultimately depends on factors beyond any single project’s control: government relocation completion, private sector migration to the area, and infrastructure development timelines. Central Point provides reasonable terms for investors who’ve assessed these broader factors and decided the opportunity aligns with their investment strategy and risk capacity.

If you’re considering Central Point, verify the rental guarantee documentation, visit completed Eight Developments projects, and assess your own timeline and liquidity needs honestly. This isn’t a short-term play, and it requires believing that New Capital will eventually function as Egypt’s administrative and business capital. If those conditions match your investment approach, the project warrants serious evaluation.

Similar Listings

Core The Business Hub New Capital

Pixel Mall New Capital | What You Need t...

Ronza Tower New Capital | What You Need ...